Clarityinthought,intentandexecution.

100%Alignedtoyourinterest.

When interests are aligned, positive outcomes flow naturally.

Single Line of Business

Our only product is advice.

Single Source of Revenue

We DO NOT take commissions from anyone. We are a fee-only advisory practice

SEBI Registered

We are committed to the highest fiduciary standards.

OUR STRATEGIES

For Salaried Professionals

A one-of-its-kind offering. Best described as a sprint. A quick burst of activity to achieve specific objectives for salaried professionals.

Learn moreFor Entrepreneurs

Curated for founders about to enter a major liquidity event — an exit, IPO, or significant capital infusion — who need a steady, aligned hand to navigate this monumental transition.

Learn moreFor Family Offices

Validation and audit for your existing Family Office set-up — whether internal, outsourced, or a combination — to ensure the right processes, structures, and governance are in place.

Learn moreThe Foundation Behind

Serenity Wealth

The Founder

Three decades of domain expertise

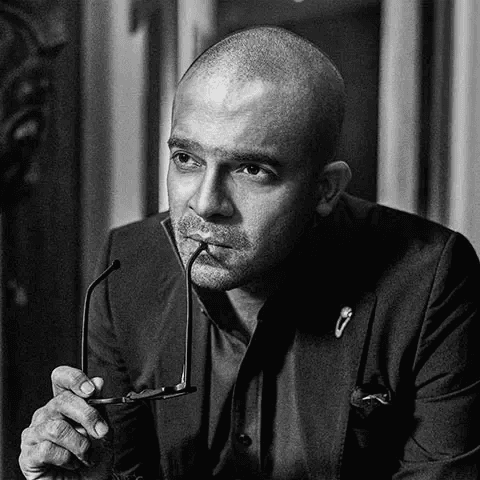

Ashish Khetan

Founder & Principal

Ashish has built a reputation defined by an unwavering obsession with client-centricity. A consummate professional who spent over two and a half decades with Kotak Mahindra Bank and pioneered the first institution-led Multi-Family Office in India in 2008.

While his background is rooted in managing high-level institutional wealth, he is driven by the conviction that professional, fee-only guidance should be accessible to all; he truly believes that every individual deserves a "slice of serenity, if not all" in their financial life.

Active Stakeholder Advisors

A strategic think-tank of multidisciplinary experts who bring diverse perspectives to our process.

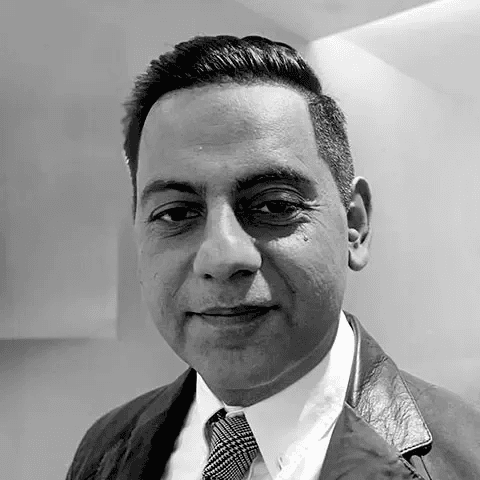

Theron Carmine De Sousa (TC)

Strategy & Brand

A 360-Degree Strategist, TC has over two decades of experience in crafting strategy and product/brand design for leading global organisations & brands; including a pivotal project helmed by the Dept of Investment and Public Asset Management (DIPAM). He graduated from Denison University, Granville, USA, with a degree in Communications and Media Strategy, followed by postgraduate studies in Sustainable Strategies.

Sahil Sadarangani

Investment & Value Creation

A serial entrepreneur with a diligent step-by-step approach to problem-solving. His mantra is: Deep Research-Deep Data Mining – Collation – Planning – Adaptive Execution, making him an expert in value creation be it for/of people, product and/or services. Sahil is a Calculus and Macro-economics major at Boston College.

The Team

Dedicated professionals across disciplines

Yash Khanna

Investment Advisor

Yash engages with individuals and families to understand their aspirations and help them build sustainable wealth through disciplined investment planning.

Tanya Singh

Media & Communication

Tanya manages communication and marketing efforts, ensuring that Serenity's philosophy and approach are clearly conveyed to clients and stakeholders.

Vivek Jindal

Analytics & Operations

Vivek combines analytics and operational excellence to drive client service delivery, ensuring every interaction reflects Serenity's commitment to excellence.

A L Rathi

Technology & AI

Brings deep expertise in technology infrastructure and investment analytics, helping Serenity Wealth leverage data-driven insights and scalable tech solutions.

S Fernandes

Technology

Builds and maintains robust technology platform infrastructure, enabling the team to deliver reliable and uninterrupted service to clients.

Serenity Circle

Trusted mentors and advisors who guide our strategic direction

Ajay Gupta

FounderCapital Foods Pvt. Ltd.

Nandan Maluste

Fmr. Kotak, Banker & Management Consultant

Shiva Viswanathan

Founder, CMO + Design Head, Catenate.io

V Swaminathan

Venture Capitalist & Independent Director, Grand Continent Hotels

Ashish Luthra

Private Equity & Venture Capitalist, Fmr. Stakeboat & Peepul Capital

Aroon Khatter

Founder, Vendekin Technologies,BusinessWorld Retail 40U40